Tax benefits: How many Chernihiv lost in six years?

The Polissya Fund of International and Regional Research within the framework of the project “Distribution of European Principles in the Field of State Aid and Public Procurement” conducted an analysis of the situation for providing tax benefits in the Chernihiv region.

During 2006-2011, tax benefits were granted on the following taxes and fees: income tax; tax on owners of vehicles and other self -propelled machines and mechanisms; Land tax; value added tax; local taxes and fees; excise duty; Fee for exploration work performed at the expense of the state budget. In 2010, after the adoption of the Tax Code of Ukraine, the tax from the owners of vehicles ceased to exist.

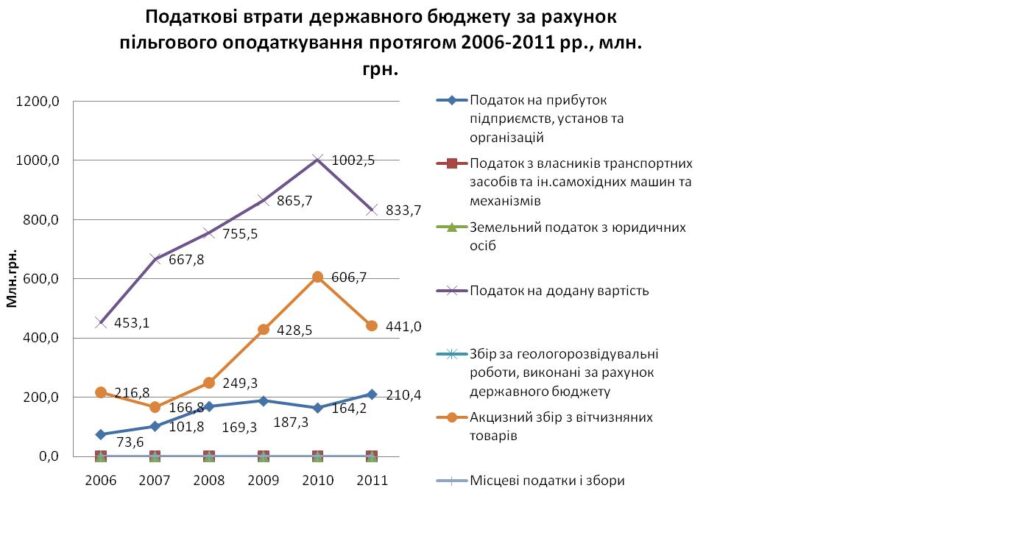

The total amount of taxes not paid to both the state and local budget tended to grow in 2006-2010. Over six years, the total losses of local budgets at the expense of providing tax benefits amounted to almost UAH 8 billion. In this case, the largest share of preferential taxation was occupied by: value added tax (58.2%); Income tax (13.8%) and excise duty (25.5%).

Due to the benefits granted in the last six years, the state budget has not received (Fig. 1): value added tax – UAH 4578.3 million; excise duty – UAH 2109.1 million; income tax – UAH 906.5 million.

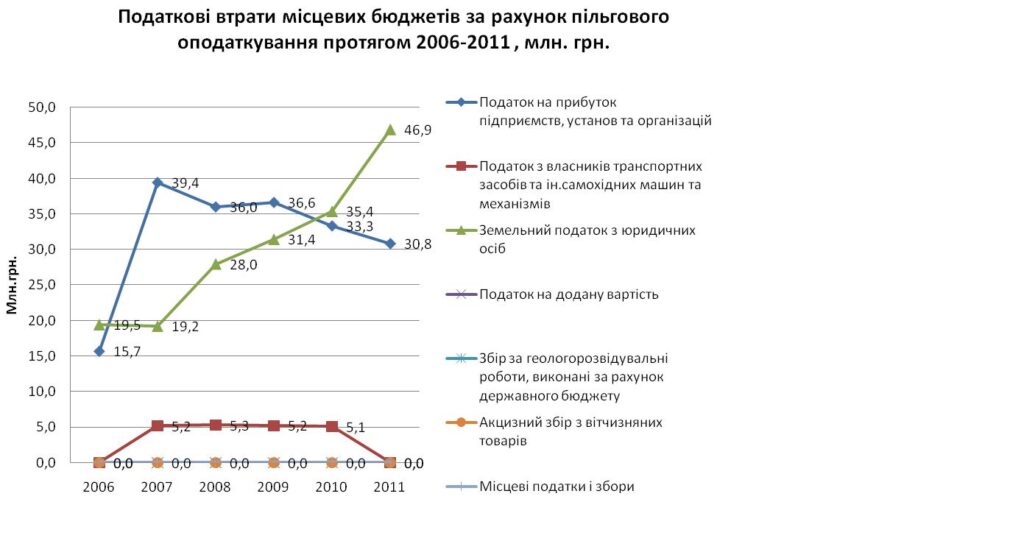

As for the local budget of Chernihiv region, the structure of the granted benefits different is slightly different. Due to the benefits granted in the last six years, the local budget has not received (Fig. 2): income tax – UAH 191.8 million; Land tax on legal entities – UAH 180.3 million; tax from owners of vehicles and other self -propelled machines and mechanisms – UAH 20.8 million.

That is, in Chernihiv region, the highest losses of the state budget are determined by granting privileges for payment of value added tax, and local – income tax on enterprises and land tax from legal entities.

In the economic and political system, tax benefits can be considered from two positions: on the one hand, it is a tool for state aid to enterprises, and on the other, a factor of unfair competition. Therefore, it is advisable to review the existing system of granting privileges and, above all, to orient it to support and development of priority sectors of the national economy. Taxes should pay everything in accordance with the legislation, and the increase in tax culture will have a positive effect on filling budgets of all levels.

Expert opinions:

Yuri Vdovenko, Director of the Chernihiv Regional Center for Investment and Development

“Tax benefits are an ambiguous tool for stimulating socio-economic development, which has both supporters and opponents. Its use is based on the fact that facilitating the conditions of conducting business in the short term and related budget losses from non -receiving funds should be overwhelmed in the long run by the effective functioning of benefits. Therefore, the macroeconomic effect of providing tax benefits can only be achieved if they are imposed with the investment activity of economic entities. During the independence of Ukraine, state policy in this area has undergone significant changes, and domestic practice showed the need to ensure transparency and economic feasibility of preferential taxation. Failure to comply with these principles will only talk about corruption and unjustified budget losses. “

Dubina Maxim, Candidate of Economic Sciences, Associate Professor of Chernihiv State Technological University

“Tax benefits are considered as a tool for stimulating the state priority sectors and economics. However, in practice in Ukraine, tax benefits are used to stimulate, primarily defined for political reasons, sectors of the national economy. This approach does not contribute to the effective use of tax benefits and does not lead to qualitative changes in the development of the national economy. For Ukraine, constant changes in the tax legislation (in 2010, the Tax Code have already been made more than 20 times different amendments), including in providing tax benefits, which makes it impossible for enterprises to develop long -term business projects and adversely affect the investment climate in the country. Investors in most cases agree to pay taxes under current legislation, however, most often complain of instability of tax legislation, which only raises their transaction costs and does not ensure confidence in the future of their own business. That is why in Ukraine, tax benefits do not perform their function, which indicates the need for a thorough revision of the tax benefit system itself. “

Maxim Koryavets, Polissya Fund of International and Regional Research

In Ukraine, the path of corruption is significantly different from the global practice – in our country all corruption methods and tools that are successful are implemented in combination with the following positive categories: public expenditures, investments, public procurement, extrabudgetary funds and institutions, tax benefits.

Therefore, the tools of tax benefits should be used as carefully and transparently as possible, as their effectiveness can be inversely proportional to increasing their volume and leading to unequal competition among enterprises and to reducing financial resources to support social infrastructure of the country and regions.

Such trends are monitored in our country, so in this period of time, the tax benefit tool should be gradually replaced by the softening of taxation conditions for all economic entities in equal volumes (reducing rates on basic national taxes), which will allow to create a full competitive environment and withdraw a significant share. Another effective option is to apply tax benefits to an entity provided that it is an investment activity, but this mechanism should be made as transparent as possible, again, to prevent certain corruption schemes.